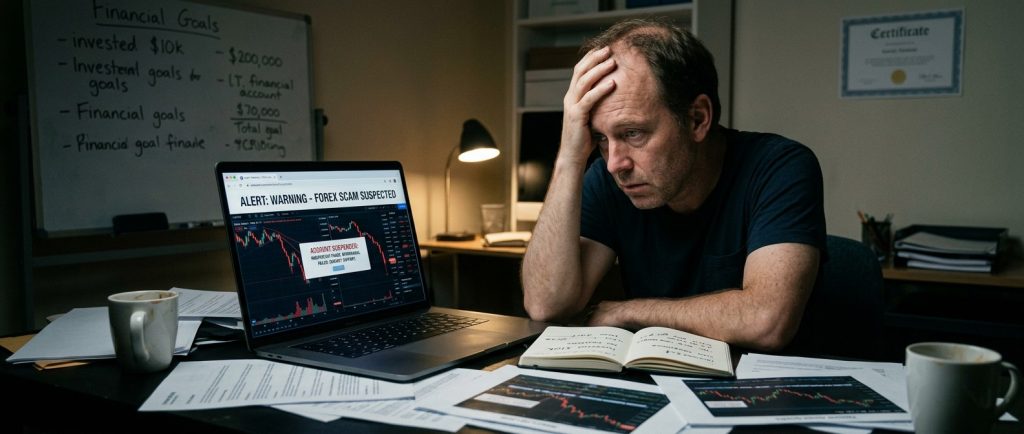

Forex scams aren’t mainly about people being naïve. They’re about using a product that already feels complicated, then adding time pressure, social proof, and a payment path that’s hard to reverse. Even traders who understand spreads, leverage, and charts can get caught because the scam sits outside the trading logic. It sits in onboarding, identity, and cash movement.

Regulators describe the pattern bluntly. The UK FCA warns about forex trading scams and specifically highlights “clone firms” that copy the details of authorised firms to look legitimate. The US CFTC warns that many online binary options platforms operate illegally and cites conduct like refusing withdrawals, identity theft, and software manipulation. Those are different products, but the scam mechanics rhyme: get money in fast, make getting money out slow, and keep the victim engaged long enough to extract more.

This article breaks down the main scam types traders run into in “forex” spaces, including intermediate scams, recovery scams, and clone site scams, and explains what to check before you believe any broker, manager, or “service” is real.

How modern forex scams are structured

Most forex scams follow a predictable structure even when the branding changes. First is the funnel. This is how they reach you: social media ads, WhatsApp invites, Telegram channels, fake reviews, influencer clips, cold calls, or job-style “account manager” outreach. Second is the trust layer. That’s where they manufacture credibility: a regulated-sounding story, screenshots of withdrawals, a friendly “senior analyst,” a fake company registration, or a cloned website that looks like a known broker. Third is the payment layer. That’s where the scam becomes hard to unwind: crypto deposits, “investment gateways,” card payments routed through processors that don’t look like brokers, or bank transfers to accounts that aren’t in the broker’s name.

What’s changed recently is speed and presentation quality. ASIC has explicitly warned that scammers are using slick website templates and plug-and-play chatbot tools to launch convincing investment scam sites quickly, and that “AI” claims are being used to add credibility. That matters in forex because the product is already digital-first, and victims expect to interact with platforms online.

A useful mental model is this: the scam is not the trading platform alone. The scam is the whole customer journey. If any part of the journey is opaque, rushed, or routed through unusual payment rails, you’re not being “offered an opportunity.” You’re being processed.

Intermediate scams

“Intermediate scam” isn’t an official regulatory term. Traders use it to describe scams that sit between obvious fraud and legitimate services. They often involve something that can exist legitimately, such as account management, signal services, copy trading, or education, but packaged in a way that is designed to extract money rather than deliver a real service.

Managed account scams that look professional

Managed forex accounts can be legitimate when done by properly licensed entities under clear rules. The scam version uses the language of asset management, “PAMM,” “MAM,” or “account management,” but avoids verifiable licensing and avoids legal clarity about who controls funds.

The common script is that you keep the account “in your name” but you must grant trading access or install software. You are shown steady profits, often small and consistent, because that feels safe. When you try to withdraw, you hit “fees,” “tax clearance,” “liquidity checks,” or “compliance verification” that require additional deposits. This is a classic escalation pattern: the first deposit is the entry price, the second deposit is the real target.

What makes this intermediate is that the early stage can look like real trading. Some scams even place real trades early to build belief. The fraud is not always the trading, it’s the control and the withdrawals.

Signal groups and “mentor” channels that are really sales machines

Signals are another grey zone. Real signals exist. The scam version is a funnel where signals are bait and the actual product is pushing you into a specific broker link, a specific “account manager,” or a specific “investment plan.”

A common tell is that the signal provider insists you must use their broker to “get the same entries.” Technically, that can be true if they’re copying trades, but in scam contexts it’s often a kickback arrangement: the signal seller gets paid when you deposit or when you trade volume, and your outcomes are irrelevant.

The risk is not only losing trades. The risk is being routed into an unregulated broker or a cloned broker environment where withdrawals become a battle.

Robot vendors and “AI bot” claims

Bots can exist. The scam is selling certainty. ASIC has called out scam platforms claiming “advanced AI trading bots” and guaranteed passive income. In forex spaces, this often looks like a bot subscription plus a brokerage account “connected” through an API or MT4/MT5 login details handed to a third party.

Two things usually go wrong. One is performance manipulation: cherry-picked backtests, curve-fitted results, or demo results presented as real. The other is operational control: the bot vendor ends up with credentials, remote access, or influence over where the money sits.

If a bot seller guarantees returns, or insists you must deposit to a specific broker, you’re no longer evaluating a strategy. You’re evaluating a cash extraction model.

PAMM and copy trading copycats

PAMM and copy trading are legitimate structures in some regulated ecosystems. The scam version uses the same vocabulary but removes the protections: no verifiable regulated entity, no audited reporting, no clear segregation of funds, and no independent dispute path.

The common trick is to show a leaderboard, a “track record,” and a community. You deposit, you see profits, then your access becomes limited or your withdrawals get blocked. The “track record” is often just a controlled display. If you cannot independently verify the provider and the legal entity, the performance numbers are not evidence.

Clone site scams

Clone scams are one of the most dangerous patterns because they defeat the basic safety habit traders are told to use: “choose a regulated broker.” The scammer does not claim to be unregulated. They claim to be the regulated firm.

The FCA explains how clone firms work: scammers use the name, address, and sometimes the firm reference number of a genuine authorised firm to convince you they’re legitimate. They then supply their own phone number, website, and contact details, sometimes claiming the real firm’s details are out of date.

How the clone works in practice

The clone can be a near-perfect copy of the real broker site, including logos, legal pages, and even PDF documents. Sometimes the clone is a lookalike domain with one character changed. Sometimes it’s an entirely different brand but with a footnote claiming regulation under a known firm’s details.

The operational aim is simple: you look up the broker, see that the real firm is authorised, and stop thinking. The scammer wants you to verify the real firm and then pay the fake one.

This is why checking “is this broker regulated” is not enough. You must check “am I dealing with the same firm that is regulated.”

Why normal due diligence fails

Clone scams exploit how people actually verify. Traders often Google the firm name and click the top result. That can be an ad placed by the scammer. Traders might also check a regulator register but then contact the firm using the phone number or email provided by the scammer, not the phone number on the regulator’s register.

The FCA explicitly warns that clone firms may claim the genuine firm’s contact details on the FCA register are out of date. That’s a direct callout of the “verification loop” trick: redirect the victim away from the authoritative contact channel.

What clone victims often experience

Clone victims often experience “normal” onboarding. They may even see a platform that behaves plausibly. The reveal happens at withdrawal. The scammer adds friction, invents fees, requests more deposits, or simply stops responding.

This pattern is not limited to the UK. Clone scams exist globally. The UK FCA publishes a warning list and clone guidance because it’s frequent enough to be a recurring consumer threat.

Recovery scams

Recovery scams are the second wave. They target people who have already lost money. That makes them brutally efficient, because the victim is already emotionally invested and wants a fix.

The CFTC describes recovery frauds as re-victimization and warns that legitimate government agencies will never ask you for money, and will only use “.gov” email addresses. In plain terms, anyone promising to “recover your funds” for an upfront fee is almost always running the next scam.

How recovery scammers find you

Recovery scammers often buy victim lists, scrape complaint forums, or contact people who posted on social media about a loss. Sometimes the “recovery firm” is the same group that ran the original scam, wearing a different mask. You get an email saying your funds were traced, frozen, or located. You just need to pay a “release fee,” “court fee,” “tax,” or “blockchain verification cost.”

The recovery scam payment logic

Recovery scams often demand payment through crypto, gift cards, or bank transfers to unrelated entities. They may claim to be lawyers, investigators, or regulators. They may use fake documents and case numbers. They will usually create urgency by saying the funds will be released only if you act within a short window.

Regulators and supervisors have also warned about the role of remote access tools in these scams. Luxembourg’s CSSF warns about the risks of installing remote access software, noting it is frequently used by fraudsters in investment and recovery scams. This is a common move: the “recovery agent” wants access to your computer to “help,” and then uses it to access your bank, email, or crypto wallet.

Why people fall for recovery scams

People fall for recovery scams because the first scam created a painful gap between “account balance on screen” and “cash in bank.” Recovery scammers promise to close that gap. They also exploit shame. Many victims don’t want to go to police or regulators. The scammer offers a private solution.

The correct assumption is harsh but practical: if someone cold-contacts you offering recovery, they are almost certainly trying to extract more money. Real recovery work is slow, document-heavy, and rarely involves guarantees.

Other common patterns that sit around forex scams

Forex scams often blend categories. These patterns show up across intermediate, clone, and recovery scams.

Remote-access theft disguised as “support”

Remote-access tools are used to “help you install the platform” or “help you withdraw.” Once installed, the scammer can watch you log in, change details, or initiate transfers. CSSF’s warning about remote access software being used by fraudsters is directly relevant here. This is also why legitimate brokers rarely require remote access. They can guide you without taking control of your device.

Bonus traps and withdrawal conditions

Some scam brokers offer large bonuses that look like free money, then attach withdrawal conditions like volume requirements, “verification fees,” or arbitrary compliance steps. Real brokers can have promotional terms too, but regulated firms usually disclose them clearly and do not invent new fees at the point of withdrawal. In scam setups, the bonus is a hook that becomes a chain.

“Liquidity provider” and “tax” stories at withdrawal

A very common withdrawal obstruction is a story that sounds technical: liquidity provider approval, AML verification fees, tax clearance, or “wallet validation.” The goal is to turn a withdrawal request into a new deposit request. The moment a broker or manager says you must deposit more money to withdraw your own money, you should assume the funds are not coming back through normal channels.

The binary options overlap

Even if your topic is “forex,” many scams route victims into binary-style products or “digitals.” The CFTC’s binary options fraud warning highlights unregistered platforms denying withdrawals and manipulating software. The product changes, the tactics don’t: easy onboarding, flashy returns, withdrawal friction.

How to protect yourself in practice

Protection comes down to verification and payment discipline. Verification means you identify the exact legal entity, confirm it on the regulator’s own register, and only use contact details found on that register, not in an email, ad, or WhatsApp message. FCA guidance on clone firms exists because looking up a firm name alone is not enough. Payment discipline means you treat irreversible payment rails as a one-way door. If someone insists on crypto transfers to “activate” your account or to “unlock withdrawals,” you should assume you’re funding a scam.

If you think you’ve been targeted, stop sending money, stop installing software, stop sharing documents beyond what you’ve already given, and move communications to written channels you control. If remote access was installed, treat the device as compromised and change passwords using a clean device. Regulator and agency guidance on recovery frauds is clear that agencies won’t ask you to pay to get money back.

If you want this tailored, tell me your country and the broker or platform name you’re seeing, and I’ll outline the exact verification path using the relevant regulator registers and the common impersonation tricks used in that region.